Issue 6 of my newsletter – subscribe here

Since buying a house a couple of years ago, I’ve noticed more and more people talking about overpaying their mortgages, and I find the whole idea mystifying.

The mechanics of mortgages were alien to me until recently, and they may well be to you as well. In the UK, most people opt for 25 year mortgages with a reasonably substantial deposit, usually around 5-10% of the value. For the first few years, the interest rate on the mortgage will be higher because your loan-to-value ratio will also be higher – that is, the amount you’ve borrowed vs. the value of your house. That means your monthly mortgage payments will also be relatively high.

But as time goes on and your mortgage payments add up, the amount you’ve borrowed will decrease. More importantly, the value of your house has probably gone up. In some areas, it might have gone up a lot. That means your loan-to-value ratio will be lower, so banks will trust you more and offer you a significantly lower rate of interest if you remortgage. Right now, you could get as low as 2% interest on your mortgage, vs. the 4+% at the start of your mortgage.

It doesn’t sound like a big difference, but when you’ve borrowed hundreds of thousands of pounds, it adds up to hundreds of pounds per month in increased mortgage payments. I was genuinely shocked by how much our mortgage payments decreased after just two years when we remortgaged for a lower rate, and I thought I was financially savvy.

Anyway – that’s all prologue to the fact that for many homeowners, when their mortgage payments decrease, they decide to overpay their mortgage, sometimes by a significant amount. If you overpay each month, you could clear your mortgage years earlier than its default 25 year term.

The act of overpaying a mortgage, I believe, confers such a strong feeling of security and responsibility and satisfaction that many very smart people will prioritise mortgage overpayments over every other form of investment. At least, that’s the only way I can explain such a mystifying decision.

Now, it is true that Money Saving Expert, the middle-class bible, tells you to overpay your mortgage, assuming you have no other higher-interest debts. Why? Their answer is that while the interest rate on mortgages can be very low, most savings rates are even lower. It’s possible to beat 2% on a few savings products like Cash ISAs and fixed-rate accounts where you lock your money away for a year or more, but I suspect most people are not using those.

So far, so sensible. It’s only until you get to the end of the long article that it explores alternatives to saving, like investing, with the stark warning:

But to generate the amount of investment returns equivalent to paying off your mortgage, you’d usually need relatively high-risk investments – overpaying the mortgage gives a surety of return.

This is a brilliant summation of British distrust in the stock market, and specifically index funds, which are the one of the more accessible alternatives to traditional savings and bonds. Index funds are the opposite of traditional wheeler-dealer stock traders – they’re composed of shares that mirror the biggest companies in a particular market, and those shares only get bought and sold as those companies gradually get bigger or smaller.

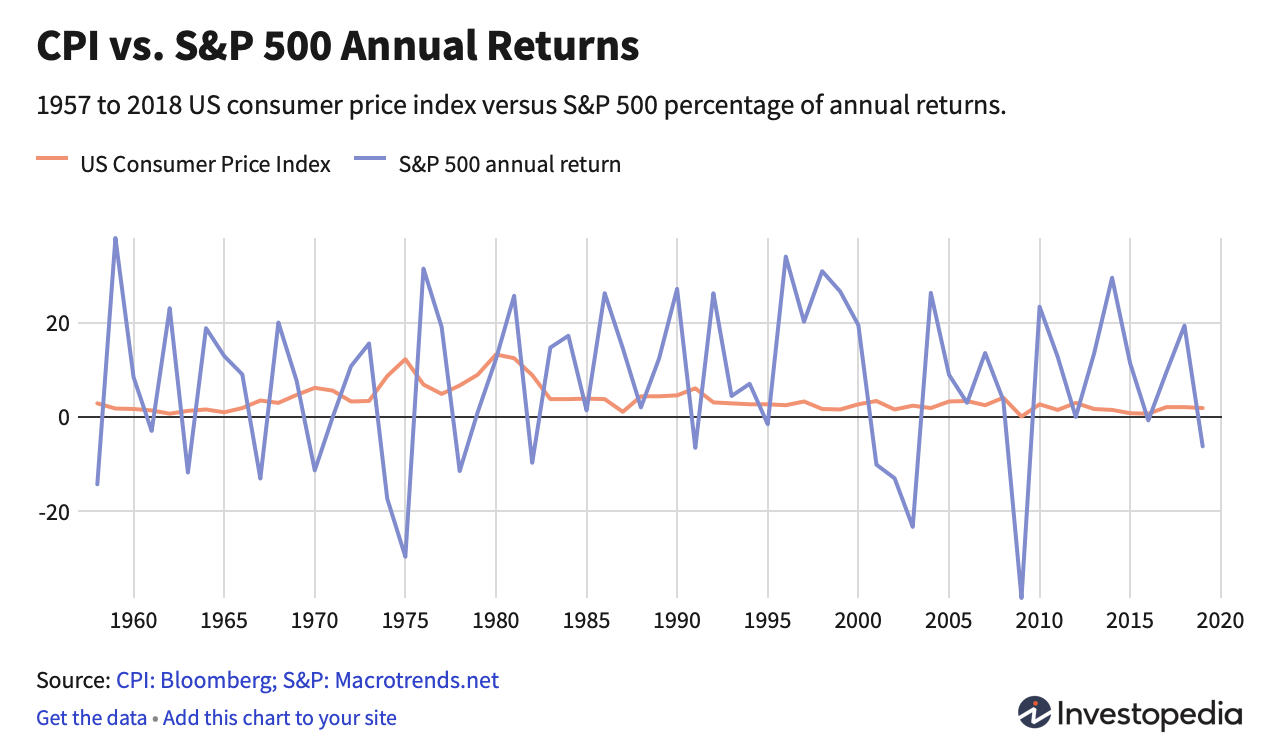

Still, index funds are volatile: their price can jump up and down in just a few days. In bad years, an index fund might lose as much as 40% of its value, as happened in 2008. On the face of it, it’s no surprise people distrust the stock market. And because it’s plainly risky to put your money in index funds in the short term, many people think it’s even riskier to do that for the long term.

The truth is completely different. Index funds are much less risky if you hold them for the long term. The average rate of return from the S&P 500 index (a bundle of major US companies) over last 60 years is 7%, after you’ve taken inflation into account.

In some years, the index has dropped a huge amount, but most years it’s increased. And the longer you hold an index fund for, the more those dips and spikes are evened out, such that you don’t need to worry about timing. Here’s an extreme example:

Imagine you were spectacularly unlucky and you invested in the S&P 500 on August 9th 2007, the day before it began its massive year-long crash. Two years later, you would have lost 47% of your money: a dire result. But if you held on to your money until 2017, you’d have realised a gain of 6% per year, after inflation – far higher than any interest rate you’d get from savings or bonds.

Most financial advisors agree that index funds are one of the best choices for investment, and they would undoubtedly favour them over overpaying a mortgage with a 2% interest rate. So why do people distrust them so much?

- Index funds don’t make investment firms a lot of money, so they prefer to advertise and promote actively-managed investment funds whose managers buy and sell shares much more faster. As famously demonstrated by a $1 million bet by Warren Buffet, these funds tend to underperform index funds over the long term, but due to survivorship bias you often just hear about the funds that succeeded rather than the ones that failed.

- At school, the only thing I learned about the stock market was the Great Depression. You just can’t underestimate the importance of education in all of this.

- Likewise, popular culture associates the stock market with risk-taking wheeler dealers. It’s basically gambling.

All of this is a great shame, because it makes people poorer. You might say, boo hoo, what a shame that people fortunate enough to own a house aren’t making more money. OK, fine, but until we get rid of capitalism, I think it’d be a good thing for more normal people to own part of large companies and benefit from their profits. Right now, those gains are disproportionately going to the wealthy.

I personally wouldn’t put all my savings into index funds due to their volatility. But while home prices aren’t as volatile, they are highly illiquid in that you can’t quickly turn a bit of your house into cash if you need it. And of course, the volatility of the stock market is lessened if you view it over the term of a 25 year mortgage.

It suits the financial industry that homeowners remain so risk-averse and financially ignorant that they harm themselves. I wish more people would consider index funds over mortgage overpayments. But it’s hard to change the stubborn British belief that housing is the best, and only, investment normal people can make.

—

Today, Microsoft launched the Xbox Games Pass (basically, Netflix for games) at $5/month on PCs, joining the existing console-only Games Pass for $10/month, and the “Ultimate” Games Pass that combines both and adds a few extras on top for $15/month.

This makes me think the Apple Arcade subscription price is going to be lower than most people expect. Apple has a reputation for being expensive, but their subscription products are comparable with competitors:

- Music: Apple Music, Spotify, and Google Play Music are all $10/month

- Storage: iCloud Drive and Google One both offer 200GB for $3/month

- Apple News+ is the same $10/month as Texture was before Apple acquired it

Apple Arcade is interesting because it extends across iPhone, iPad, Apple TV, and Macs – but it probably has fewer AAA titles and blockbuster IPs than Xbox Games Pass. So if I had to guess, I’d say it’ll land at $7/month – far less than the $15/month some commentators have floated.

Maybe an “Apple Prime” that includes games, news, music, storage, and AppleCare for $30-40/mo?

Playing

🎮 Kids on iPad. 30 minutes of weird, mesmerising, disturbing interactive animation about crowds, groupthink, and kids.

Watching

📺 When They See Us on Netflix about the Central Park Five. One of the best things I’ve seen this year; excellent acting and beautiful direction. I couldn’t get through the final episode without crying.

Reading

📖 The Soul of a New Machine by Tracy Kidder. My book of the year so far; full thoughts next week.

📖 Saga, Volume 1 by Brian K. Vaughn and Fiona Staples. Entertaining epic sci-fi/fantasy comic. Didn’t quite live up to the “better than Star Wars” hype, but hey, it was on Libby from my library so why not? ¯_(ツ)_/¯

📖 9 Lessons in Brexit by Ivan Rogers, the former UK ambassador to the EU. A very short book, more like an extended essay really, about misconceptions the British have about the EU and Brexit process. A tad overwritten, but that’s civil servants for you.

My main takeaway is that the government’s prioritisation of immigration and goods trade over services (which are worth far more to the UK economy) is going to majorly bite us on the arse.

📰 The Wild West Meets the Southern Border by Valeria Luiselli in the New Yorker, about the parallels between Wild West re-enactors in Tombstone and US attitudes towards the border with Mexico. Very enjoyable and insightful. Here’s a bit that, perhaps deliberately, reminded me of the modern Westworld:

The town, it seemed, existed not only in a loop of embodied repetitions of odd historical moments but also in a kind of cut-and-paste of the same people. It is entirely possible that, at any given moment in Tombstone, Wyatt Earp is having a beer with Wyatt Earp.

and on re-enactors’ fetish for details over the big picture:

An interesting paradox of the reënactment scene’s obsession with authenticity and historical accuracy, this “getting it right,” is that accuracy is measured in terms of the minute details of a particular event, which does not necessarily amount to historical accuracy in the broader sense. Old West history buffs may endlessly dispute whether Wyatt Earp was wearing a specific kind of bow tie during the O.K. Corral shoot-out in 1881, but may be oblivious of much of what was happening in the region during those years.

Visiting

🎤 Cymera, “Scotland’s Festival of Science Fiction, Fantasy and Horror Writing”.

Some choice (paraphrased) quotes from Ken MacLeod:

“Hard science fiction” is anything you can honestly sell with a spaceship on the cover. “Space opera” is anything you can honestly sell with an exploding spaceship on the cover.

… Space opera is justified because it’s the most optimistic form of science fiction. It shows we still have a future. And it gives us a vast arena for recreating mythological adventures.

Charlie Stross:

“Horror” is about loss of control. About the loss of bodily autonomy.

🏛️ I saw the Edinburgh (University) College of Art graduate show and the Edinburgh College HND show yesterday.

Lots of interesting art but my eyes were left bleeding from the blizzard of spelling mistakes and typos. Spelling errors in titles. Flagrant abuse of apostrophes. Grammatical errors every page. Barely any project was immune. It was painful to read.

I understand students might think they’re here to be artists, not writers – but unless you’re the best of the best, it’s really important to have a rounded set of skills.